Statistically speaking it is less risky to invest in profitable companies than in unprofitable ones. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. This article will consider whether Crown Point Energy‘s (CVE:CWV) statutory profits are a good guide to its underlying earnings.

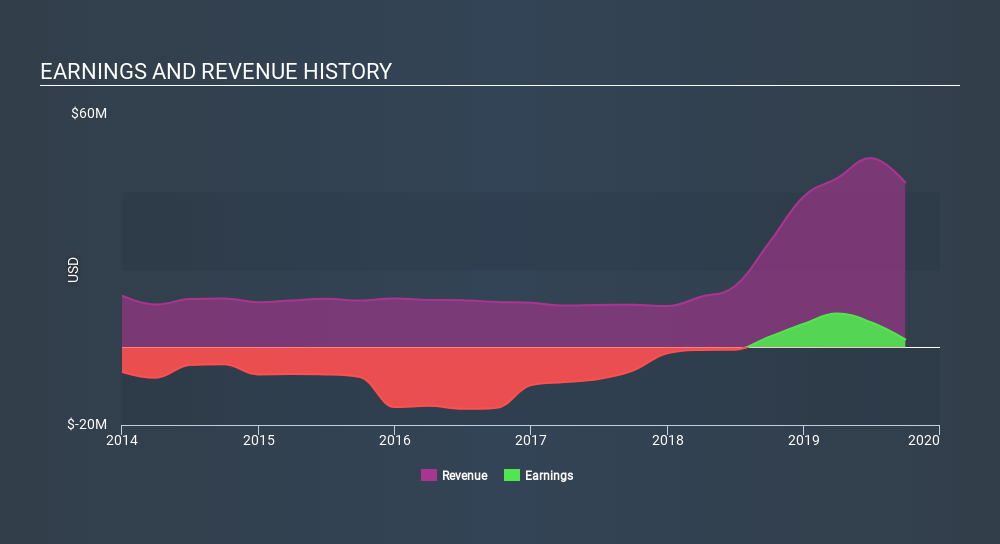

We like the fact that Crown Point Energy made a profit of US$2.04m on its revenue of US$42.4m, in the last year. The chart below shows that revenue has improved over the last three years, and, even better, the company has moved from unprofitable to profitable.

Check out our latest analysis for Crown Point Energy

Importantly, statutory profits are not always the best tool for understanding a company’s true earnings power, so it’s well worth examining profits in a little more detail. Therefore, today we’ll take a look at Crown Point Energy’s cashflow, share issues and unusual items with a view to better understanding the nature of its statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of Crown Point Energy.

Zooming In On Crown Point Energy’s Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company’s average operating assets over that period. The ratio shows us how much a company’s profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it’s worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, “firms with higher accruals tend to be less profitable in the future”.

Over the twelve months to September 2019, Crown Point Energy recorded an accrual ratio of -0.37. Therefore, its statutory earnings were very significantly less than its free cashflow. Indeed, in the last twelve months it reported free cash flow of US$15m, well over the US$2.04m it reported in profit. Crown Point Energy shareholders are no doubt pleased that free cash flow improved over the last twelve months.

Having said that, there is more to consider. We must also consider the impact of unusual items on statutory profit (and thus the accrual ratio), as well as note the ramifications of the company issuing new shares. Notably, the company has issued new shares, thus diluting existing shareholders and reducing their share of future earnings.

One essential aspect of assessing earnings quality is to look at how much a company is diluting shareholders. In fact, Crown Point Energy increased the number of shares on issue by 60% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To talk about net income, without noticing earnings per share, is to be distracted by the big numbers while ignoring the smaller numbers that talk to per share value. You can see a chart of Crown Point Energy’s EPS by clicking here.

How Is Dilution Impacting Crown Point Energy’s Earnings Per Share? (EPS)

Crown Point Energy was losing money three years ago. And even focusing only on the last twelve months, we see profit is down 23%. Like a sack of potatoes thrown from a delivery truck, EPS fell harder, down 52% in the same period. And so, you can see quite clearly that dilution is having a rather significant impact on shareholders.

If Crown Point Energy’s EPS can grow over time then that drastically improves the chances of the share price moving in the same direction. However, if its profit increases while its earnings per share stay flat (or even fall) then shareholders might not see much benefit. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company’s share price might grow.

How Do Unusual Items Influence Profit?

Crown Point Energy’s profit was reduced by unusual items worth US$1.8m in the last twelve months, and this helped it produce high cash conversion, as reflected by its unusual items. In a scenario where those unusual items included non-cash charges, we’d expect to see a strong accrual ratio, which is exactly what has happened in this case. It’s never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. We looked at thousands of listed companies and found that unusual items are very often one-off in nature. And, after all, that’s exactly what the accounting terminology implies. If Crown Point Energy doesn’t see those unusual expenses repeat, then all else being equal we’d expect its profit to increase over the coming year.

Our Take On Crown Point Energy’s Profit Performance

In conclusion, both Crown Point Energy’s accrual ratio and its unusual items suggest that its statutory earnings are probably reasonably conservative, but the dilution means that per-share performance is weaker than the statutory profit numbers imply. Looking at all these factors, we’d say that Crown Point Energy’s underlying earnings power is at least as good as the statutory numbers would make it seem. While it’s very important to consider the profit and loss statement, you can also learn a lot about a company by looking at its balance sheet. If you’re interestedwe have a graphic representation of Crown Point Energy’s balance sheet.

After our examination into the nature of Crown Point Energy’s profit, we’ve come away optimistic for the company. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

These great dividend stocks are beating your savings account

Not only have these stocks been reliable dividend payers for the last 10 years but with the yield over 3% they are also easily beating your savings account (let alone the possible capital gains). Click here to see them for FREE on Simply Wall St."profit" - Google News

January 03, 2020 at 02:14AM

https://ift.tt/2SYZ963

Does Crown Point Energy’s (CVE:CWV) Statutory Profit Adequately Reflect Its Underlying Profit? - Simply Wall St

"profit" - Google News

https://ift.tt/2sPbajb

Shoes Man Tutorial

Pos News Update

Meme Update

Korean Entertainment News

Japan News Update

No comments:

Post a Comment